et et lorem labore dolore incididunt tempor incididunt consectetur incididunt

Regional markets – Expect uncertainty as geopolitics and oil policy set the tone

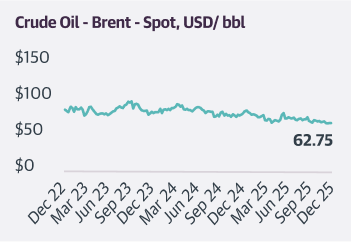

Regional markets enter the first full trading week of 2026 with a geopolitical bang, setting an uncertain tone at the start of the year. The weekend overthrow of Venezuela's President Nicolás Maduro introduces headline risk and raises the likelihood of some oil price volatility in the near term. Venezuela's current oil production remains limited at below 1 million barrels per day, or under 1% of global supply. With global oil markets oversupplied and first-quarter demand seasonally weak, near-term pricing remains anchored in producer policy. As a result, attention turns to today's OPEC+ meeting, where guidance on supply is expected to set the direction for crude prices this week.

Global markets – Macro data to drive growth and interest rate expectations

Global markets face an active start to the year as macro data shape expectations for growth and monetary policy. In the US, the non-farm payrolls report will guide views on labour- market momentum and the Federal Reserve's policy path. In Europe, euro-area PMI and confidence indicators may clarify whether activity stabilised after a weak end to 2025. In Asia, China's manufacturing PMI and trade balance will shape expectations for demand, exports, and commodities. Thinner liquidity following the holiday period could amplify market reactions across asset classes.

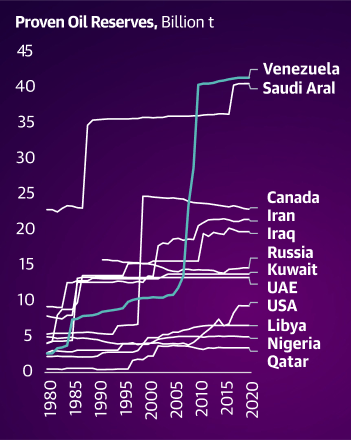

Note to Management – Prioritise OPEC+ signals over Venezuela headlines

Venezuela holds the world’s largest proven oil reserves at approximately 414 billion barrels, ahead of Saudi Arabia, Canada, and Iran (see chart RHS). While this establishes Venezuela as a long-term supply optionality story, current production constraints mean it has limited influence on near-term oil balances. Oil markets have largely priced in Venezuela’s low output, with oversupply, elevated inventories, resilient US shale production, and OPEC+ policy continuing to weigh on prices. Any immediate price response to recent events is expected to be modest unless physical disruptions materially exceed expectations. With demand soft into early 2026, coordinated supply policy from OPEC+ remains the dominant driver of oil prices, with meeting outcomes and guidance likely to matter more than Venezuela-related developments in the near term.

| IR & Beyond | ||

| Reuters | Global equity funds see strong inflows in final week of 2025 | Link |

| HBR | Leaders, Bring Your Best Self into the New Year | Link |

| Business today | Tech and AI predictions 2026: From AI-led job freeze to rise of AI agents | Link |

| CNBC | Payment giants are preparing a world where AI book flights & shop… | Link |

| Investing.com | Market Volatility Strategies for Investors | Link |

Last week in the GCC, Bahrain (+0.1%) partly recovered its prior week loss. Saudi Arabia (+0.2%) extended its gain as the country’s National Debt Management Center said it completed arrangements for a $13 billion loan to help finance power, water and public utilities projects. Dubai (-0.3%) ended a five weeks rising streak, hit by losses in real estate and banking stocks. Abu Dhabi (-0.4%) and Qatar (-0.4%) clocked identical losses. Qatar was weighed down by selling pressure from both foreign retail and institutions. Kuwait (-0.8%), and Oman (-1.0%) reversed their gains.

US markets fell last week. The Nasdaq Composite (-1.5%) slid the most, followed by the S&P 500 (-1.0%), and the Dow (-0.7%). Profit booking, a pullback by technology stocks, and latest FOMC minutes showing mixed views on interest rates outlook resulted in market weakness. In Europe, the DAX (+0.8%) rose for a sixth successive week, STOXX600 (+1.3%) advanced, while FTSE100 (+0.8%), and CAC40 (+1.1%) recovered their losses.

| 10 Most Read Regional Sector Headlines | |

| Insurance | QIC crowned as 'Best General Insurance Company' in Qatar |

| Telecom | Oman Broadband aims to connect 1mn homes with fiber-optic network |

| Energy | Oman's OETC powers ahead with grid expansion and green growth |

| Aviation | Aviation sector contributes $1.8bn to Oman’s GDP |

| Infrastructure | Riyadh announces $2bn main ring road axes development programme |

| Banking | Saudi central bank mandates 25 free services to boost customer protection |

| Technology | Saudi Arabia: Huawei Cloud shares strategy, strengthens partner network |

| Transportation | Dubai's RTA activates e -scooter permit application service |

| Healthcare | Oman advances participatory health planning under Vision 2040 |

| Construction | Work starts on 35 -km green corridor at King Salman Park |

| 10 Most Read Regional Company Headlines | |

| e& | e& and ZTT complete region’s first hollow -core fibre field trial |

| Tuba | Tuba joins NVIDIA Inception for AI innovation in healthcare |

| Tuwaiq Academy | Tuwaiq Academy celebrates 15 years of transformative education |

| Emirates | Emirates carries 55.6mn Passengers in 2025 |

| AmiViz | AmiViz to introduce QuilrAI’s AI security portfolio in Middle East |

| Azizi | UAE: Azizi’s premium project in Riviera 65% complete |

| Maaden | Maaden teams up with Hancock for Saudi mining exploration JV |

| Ooredoo | Ooredoo signs research MoU with GORD on sustainability roadmap |

| ACWA Power | ACWA Power agree to acquire stake in 5 wind power projects in China |

| Taqa | Taqa and Ewec complete $980 million Al Dhafra power plant deal |

| Macro Calendar | |

| 04 Jan 2026 | US Fed's Paulson speech |

| 05 Jan 2026 | China RatingDog Services PMI (Dec) |

| 05 Jan 2026 | US ISM Manufacturing PMI (Dec) |

| 06 Jan 2026 | Germany Consumer Price Index (YoY) (Dec) |

| 07 Jan 2026 | Eurozone Core Harmonized Index of Consumer Prices (MoM) (Dec) |

| 07 Jan 2026 | Germany Retail Sales (YoY) (Nov) |

| 07 Jan 2026 | US ADP Employment Change (Dec) |

| 08 Jan 2026 | Switzerland Consumer Price Index (YoY) (Dec) |

| 09 Jan 2026 | China Consumer Price Index (YoY) (Dec) |

| 09 Jan 2026 | Eurozone Retail Sales (YoY) (Nov) |

| Markets | Last Close | YTD % | QTD % | MTD % | MCap (bn) | P/E | P/B |

| Saudi Arabia | 10,549 | 0.6% | 0.6% | 0.6% | $2,387 | 17.8x | 2.1x |

| ADX | 9,995 | 0.0% | 0.0% | 0.0% | $764 | 19.7x | 2.5x |

| DFM | 6,114 | 1.1% | 1.1% | 1.1% | $255 | 10.0x | 1.8x |

| Nasdaq Dubai | 4,889 | 0.7% | 0.7% | 0.7% | $140 | 9.9x | 1.5x |

| Qatar | 10,763 | 0.0% | 0.0% | 0.0% | $156 | 12.1x | 1.3x |

| Bahrain | 2,067 | 0.0% | 0.0% | 0.0% | $21 | 14.2x | 1.4x |

| Oman | 5,896 | 0.5% | 0.5% | 0.5% | $34 | 9.6x | 1.3x |

| Kuwait | 8,908 | 0.0% | 0.0% | 0.0% | $173 | 16.2x | 1.8x |

Sources: Energy Institute - Statistical Review of World Energy (2025), S&P Capital IQ Pro, Iridium Advisors Analysis

Disclaimer: Iridium Advisors uses artificial intelligence tools that can make mistakes. The information provided in this newsletter is for information purposes only and should not be construed in any way as business, financial or investment advice nor as a recommendation to buy, sell, or hold any particular security. Iridium Advisors believes the information in this newsletter to be accurate, but does not verify its accuracy, timeliness, completeness for any particular purpose and/or non-infringement. Iridium Advisors does not bear any responsibility whatsoever to provide any updates, corrections or changes to the information in this document, nor will it accept liability for any damages or losses in connection with the use of this document. ©Copyright 2025, Iridium Advisors. All rights reserved.

| Commodities | WTD | YTD |

| Oil (WTI) | 1.02% | -0.17% |

| Oil (Brent) | 0.18% | -0.16% |

| Gold | -4.43% | 0.30% |

| Natural Gas | -17.13% | -1.84% |

| Asset Class Monitor | WTD | YTD |

| Bitcoin | 2.79% | 2.74% |

| Aluminium | 2.79% | 2.74% |

| MSCI EM | 2.30% | 1.79% |

| FTSE 100 | 0.82% | 0.20% |

| US Treasury | 0.27% | -0.54% |

| MSCI GCC | -0.09% | 0.44% |

| MSCI World | -0.31% | 0.49% |

| S&P 500 | -1.03% | 0.19% |

| Leaderboard | MCap (bn) | WTD | YTD |

| Aramco | $1,541 | 0.3% | -15.0% |

| IHC | $239 | 0.0%/td> | -1.4% |

| Rajhi | $104 | 0.4% | 3.1% |

| TAQA | $99 | -4.5% | -4.0% |