Iridium IR Brief No. 454 - What's Next for GCC Markets - 28 June 2026

Markets turn cautious as attacks on Bahrain and two vessels renew escalation concerns

The Week Ahead

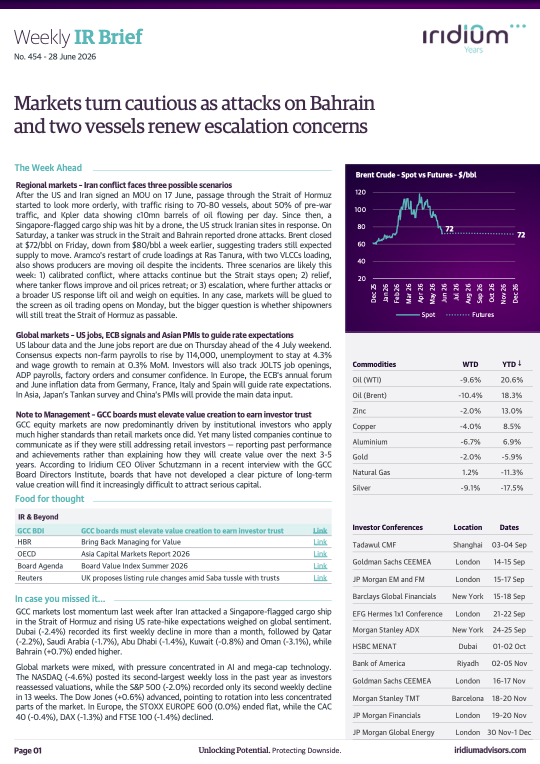

Regional markets – Iran conflict faces three possible scenarios

After the US and Iran signed an MOU on 17 June, passage through the Strait of Hormuz started to look more orderly, with traffic rising to 70-80 vessels, about 50% of pre-war traffic, and Kpler data showing c10mn barrels of oil flowing per day. Since then, a Singapore-flagged cargo ship was hit by a drone, the US struck Iranian sites in response. On Saturday, a tanker was struck in the Strait and Bahrain reported drone attacks. Brent closed at $72/bbl on Friday, down from $80/bbl a week earlier, suggesting traders still expected supply to move. Aramco’s restart of crude loadings at Ras Tanura, with two VLCCs loading, also shows producers are moving oil despite the incidents. Three scenarios are likely this week: 1) calibrated conflict, where attacks continue but the Strait stays open; 2) relief, where tanker flows improve and oil prices retreat; or 3) escalation, where further attacks or a broader US response lift oil and weigh on equities. In any case, markets will be glued to the screen as oil trading opens on Monday, but the bigger question is whether shipowners will still treat the Strait of Hormuz as passable.

Global markets – US jobs, ECB signals and Asian PMIs to guide rate expectations

US labour data and the June jobs report are due on Thursday ahead of the 4 July weekend. Consensus expects non-farm payrolls to rise by 114,000, unemployment to stay at 4.3% and wage growth to remain at 0.3% MoM. Investors will also track JOLTS job openings, ADP payrolls, factory orders and consumer confidence. In Europe, the ECB’s annual forum and June inflation data from Germany, France, Italy and Spain will guide rate expectations. In Asia, Japan’s Tankan survey and China’s PMIs will provide the main data input.

Note to Management – GCC boards must elevate value creation to earn investor trust

GCC equity markets are now predominantly driven by institutional investors who apply much higher standards than retail markets once did. Yet many listed companies continue to communicate as if they were still addressing retail investors — reporting past performance and achievements rather than explaining how they will create value over the next 3-5 years. According to Iridium CEO Oliver Schutzmann in a recent interview with the GCC Board Directors Institute, boards that have not developed a clear picture of long-term value creation will find it increasingly difficult to attract serious capital.

Subscribe

Receive our signature insights and analysis from across the firm.

More on Investor Relations

Iridium IR Brief No. 453 - What's Next for GCC Markets - 21 June 2026

Hormuz reopens as markets wait for trade flows and confidence to recover

The Week Ahead

Regional markets – Hormuz passage resumes, but caution remains

After the US–Iran MOU was signed, the Strait of Hormuz reopened and tanker traffic resumed. Oil shipments have started to recover, but flows remain below pre-conflict levels and vessels are still being asked to coordinate passage in advance. This should support risk appetite in GCC equities, although the recovery in shipping volumes, freight costs and insurance premia is likely to be gradual. Investors will also watch whether the 60-day negotiation window holds, after Saudi Arabia’s Foreign Minister warned that trust with Iran must be rebuilt before broader economic cooperation can resume.

Global markets – US PCE, PMIs and bank stress tests to guide rate expectations

Global markets will focus on US inflation, growth and banking sector signals this week. The main release will be May personal income and spending data, including the Fed’s preferred PCE inflation gauge, with core PCE expected to accelerate to 0.3% MoM from 0.2% in April. Durable goods orders are expected to fall after April’s strong increase, while preliminary S&P Global PMIs, regional Fed surveys and the third estimate of 1Q GDP will give investors a broader read on US momentum. The Fed’s 2026 bank stress test results will also be watched by financials investors. Outside the US, PMIs are due from the Euro Area, Germany, France, the UK, Japan and India, while China is expected to keep loan prime rates unchanged.

Note to Management – Investors continue to support quarterly reporting

In a letter to the SEC, the CFA Institute cited a member survey showing strong investor support for quarterly reporting. The survey found that 62% of respondents oppose replacing quarterly reporting with semi-annual reporting, while 63% believe the benefits of quarterly reporting exceed the costs. Around 70% oppose giving companies flexibility to determine or change their own reporting frequency, and nearly 85% are concerned that flexible reporting frequency and format would reduce comparability between companies. Although 82% support allowing voluntary quarterly reporting if semi-annual reporting is adopted, only 32% expect companies would continue reporting quarterly if reporting became optional. Earlier this month, the SEC’s own Investor Advisory Committee formally recommended that the SEC reject the proposal.

Iridium GEM Fund Insights - 1Q 2026

UAE and Saudi Arabia retain GEM fund allocations in a turbulent quarter

Saudi Arabia demonstrated resilience since the outbreak of the Iran war, with funds invested slightly declining to 59% during 1Q 2026 (4Q 2025: 60%) and an average fund weight of 1.19%. Fund overweight positions moderated to 10.2%.

The UAE retained its position as the most favoured GCC market, with a decline in funds invested settling at 64% (4Q 2025: 65%) and average fund weight at 1.22%. The overweight positions remained at 39%.

Real Estate and Financials maintained their leadership as the sectors with the highest fund exposure. UAE Real Estate was held by 53.3% of GEM funds, while KSA Financials were held by 50.4%.

At the individual stock level, overweight positions were led by industry leaders in the Financials and Real Estate sectors, with Emaar Properties and ADIB each recording a 1 percentage point increase in overweight positions. Aldar Properties retained the second position with a 24% overweight, followed by Al Rajhi and SNB at 20%.

Key takeaways for listed companies

Markets have swung quickly around Iran headlines, but GEM funds largely held exposure in Saudi Arabia and the UAE through 1Q. During the 1Q 26 earnings cycle, investors will focus on exposure to energy and freight costs, funding conditions, and knock-on effects on demand, margins, and working capital.

Management teams should come prepared with ranges and sensitivities, not broad statements, and be explicit on what changes in 2026 plans under different oil price and interest rate paths. Investors will ask questions on guidance assumptions, capital allocation priorities, and balance-sheet limits, and management should be available to address them directly.

Download the full report to explore the data in detail.

Sources: Copley Fund Research, Iridium Advisors Analysis

Escaping the low valuation trap

A common refrain heard in boardrooms is that our company is undervalued. Executives point to earnings growth, market expansion, and a strong balance sheet, yet the stock price remains stagnant. The assumption is often that analysts and investors are failing to see the company’s true potential, and that the market is missing something.

From a buy-side perspective, the reality is often the opposite. Many companies are not undervalued by accident - they are stuck in a pattern that limits their valuation. Institutional investors are not just looking for growth; they are looking for sustainable value creation - something that many companies struggle to demonstrate convincingly.

Why earnings growth and margins alone are not enough

For many executives, growth and margins are the ultimate measure of success. Expanding revenue, improving margins, and growing market share should, in theory, make a company more attractive to investors. Yet, time and again, companies with strong earnings trajectories fail to translate that into meaningful stock price appreciation.

The problem is that not all growth creates value. Investors are not just looking at how fast a company is growing; they are asking where that growth is coming from and whether it is generating returns above the cost of capital. A company that expands aggressively but only earns a modest return on its investments may be getting bigger, but it is not necessarily getting more valuable.

Companies that consistently attract premium valuations share a common characteristic: they generate returns on invested capital (ROIC) that exceed their cost of capital. This is the foundational metric that shows investors whether a company is creating economic value or simply recycling capital without compounding it.

A high-growth company with mediocre ROIC is unlikely to sustain its valuation premium, while a company with moderate but high-return growth is far more attractive to investors. This distinction is where many executives misread the market.

The problem with capital allocation decisions

Even companies with strong ROIC and promising growth prospects can find themselves undervalued if they misallocate capital. How a company deploys its free cash flow - whether reinvesting in high-return opportunities, making (value accretive) acquisitions, or returning cash to shareholders - has a profound impact on investor confidence.

Yet, in many companies, capital allocation decisions are often driven by tradition or influenced by large shareholder groups rather than a well-understood allocation framework. In businesses with significant family ownership, for example, the focus in boardroom discussions often shifts toward extracting capital by maximizing dividends rather than optimizing capital deployment. While dividends are important, they should not come at the expense of reinvestment when high-return opportunities exist.

From an institutional investor’s perspective, a high dividend payout can even be a red flag rather than a signal of strength. If a company is consistently returning most of its earnings to shareholders instead of reinvesting in its own growth, it signals one of two things: either the company has limited reinvestment opportunities, or management is not prioritizing long-term value creation.

Why some companies sustain their valuation premium

Institutional investors look beyond just earnings and dividends. They assess whether a company’s competitive position is defensible over time.

A company with strong ROIC today may not maintain it in the future if it lacks a sustainable competitive advantage - a moat that protects its profitability. Companies that successfully sustain their valuation premium typically have something that shields them from competition, whether it’s pricing power, brand strength, cost leadership, or regulatory advantages.

This is where many companies fail to convince investors. Their financials may look good, but investors question whether those numbers are defendable in the long run. Without a clear and well-articulated moat, even strong businesses will struggle to attract long-term investors.

The companies that get it right

A look at some of top-performing stocks reveals a pattern. These companies are not just growing, but growing in ways that reinforce their long-term value creation model.

Their success comes down to a few key factors: they maintain high and stable ROIC, they reinvest in growth areas that preserve or improve returns, they practice capital allocation discipline in word and deed, and they possess a competitive moat that protects their market position.

These companies have significantly outperformed—not because they grew the fastest, but because they grew the right way.

Breaking out of the trap

The key to escaping the low valuation trap is recognizing that investors are not only rewarding growth, but also high returns.

Executives should start by asking the right questions. Are we growing in a way that creates lasting value? Are we deploying capital efficiently, or simply expanding for the sake of it? Do we have a clear strategy for capital allocation, balancing reinvestment, acquisitions, and shareholder returns? And most importantly, can we defend our profitability in a way that protects our competitive position?

Companies that align their strategies with these investor priorities will attract the valuation premiums they seek. Those that continue to focus on growth without regard for its quality will remain frustrated by a stock price that doesn’t reflect their expectations.

Iridium Foreign Flow Analysis - May 2026

Foreign investors stay selective in May as Saudi equities attract modest inflows

May foreign flows show that investors are applying a higher risk premium to GCC equities, but they are not abandoning the region. The GCC recorded net foreign outflows of USD837 million in May, led by selling in the UAE, Kuwait and Qatar. Saudi Arabia was the exception, with modest net inflows of USD53 million.

Despite May’s outflow, GCC equities still recorded USD1.1 billion of net foreign inflows year to date. The MSCI GCC Index fell 1.1% in May to 747 points and is now down 5.7% year to date from 792 points. That is a negative market reaction, but it remains relatively contained given the severity and duration of the current conflict.

Key takeaway for listed companies

Saudi Arabia’s resilience appears to reflect market liquidity, EM index weight and lower perceived energy export risk. The market offers the largest equity opportunity set in the GCC and remains the most important regional allocation for global emerging market investors. Saudi Arabia also has pipeline capacity to export crude to the Red Sea, reducing its dependence on the Strait of Hormuz relative to several GCC peers. That does not remove geopolitical risk, but it helps explain why foreign inflows have remained concentrated in Saudi Arabia.

While a peace deal appears to be making progress, investors are still waiting for proof that the crisis is moving toward a final settlement. The ceasefire has helped limit the market reaction, but the absence of a final deal continues to weigh on foreign flows. Investors will need more than headlines alone before rebuilding exposure.

Download the full report to explore the detail.

Sources: S&P Capital IQ Pro, Stock Exchanges, Iridium Advisors Analysis

GCC boards must elevate value creation to earn investor trust

Many regional boards still believe that investor trust only stems from positive announcements. That could not be further from the truth. It comes from having a value creation track record. Investors like companies that say what they are going to do and then do it. They also want management to be honest about risks that are not immediately visible to them.

GCC BDI: How are capital market dynamics in the GCC evolving, and what trends are shaping investor behaviour today?

Schutzmann: I think GCC equity markets have changed quite profoundly over the past two decades.

When I arrived in the UAE in 2006, regional markets were local markets. They were mainly influenced by domestic liquidity and retail investors. That began to change when the UAE, Qatar, Kuwait and Saudi Arabia entered the Emerging Markets indices because that brought the region into the spotlight of international institutional investors who had largely seen the GCC as a source of capital, not a destination of capital.

Over the past five years alone, we’ve seen tens of billions of US dollars in cumulative net foreign inflows into GCC markets, with Saudi Arabia and the UAE receiving the largest share.

So, this is no longer only a story about local money. The daily trading activity is now largely driven by international institutions. For instance, in FY2025, nearly 40% of traded value in Saudi Arabia was attributable to foreign institutions.

In a retail market, companies can get away with hiding behind the veil of “no comment” or PR spin in quarterly results. But in an institutional market, investors have completely different standards. They want to know if a company has growth potential, if management can generate returns in excess of the cost of capital, if management can be trusted to invest in growth and return the appropriate amount of capital, and whether management does what it promised it would do.

The last change is probably the most interesting one. The market itself is forcing GCC companies to mature. Until recently, many behaved more like private companies that happen to be listed. They engaged episodically and expected investors to work out the investment case on their own.

We are starting to see more companies look and behave like mature global companies. These developments represent meaningful progress toward the standards expected in developed markets.

GCC BDI: From your perspective, what drives investor confidence in the region’s current environment?

Schutzmann: Trust is everything. Investors need to trust the business model and the management team. That immediately becomes visible in times of distress.

When markets are relatively calm, investors can focus on growth stories, dividends and the broader regional opportunity. When there is a geopolitical shock, they will ask some really difficult questions, including: Will your business keep operating? How exposed are your margins and cash flows? How long will liquidity last? How quickly will management change its capex plans, leverage or dividends if the business landscape deteriorates further?

Many regional boards still believe that investor trust only stems from positive announcements. That could not be further from the truth. It comes from having a track record.

Investors like companies that say what they are going to do and then do it. They want management to be honest about risks that are not immediately visible to them. They dislike broad reassurances because the chances are that investors have seen a similar playbook somewhere else and know how that ends.

That is why many companies lose investor trust when they delay bad news, react like a deer in the headlights to every headline, and try to manage their daily share price with positive statements. That creates the impression that management is not in control.

Companies that build trust do the opposite. They engage early, use public forums like analyst calls to explain the decisions they are making, they highlight the risks and demonstrate how the business will endure longer periods of volatility.

GCC BDI: How should boards position their organisations to remain attractive to both regional and international investors?

Schutzmann: I think boards need to hold up a mirror and ask a simple question. Would an investor understand why this company deserves their money if they looked at it for the first time?

Many companies in the region have fundamentally strong businesses, but they don’t always know how to translate that strength into a convincing investment case. They report quarterly results, announce strategic milestones after they’re laready met, but they wrestle with explaining long-term value creation and painting an accurate picture of where the business will be in 5 or 10 years.

For boards that means capital markets positioning has to go beyond regulatory disclosures. The most advanced GCC companies, for example Saudi banks, give investors a framework. They portray an accurate picture of the bank in the future, explain their strategic, financial and operational roadmap and report detailed progress every quarter. That allows investors to confirm or discredit their investment thesis.

Boards should position their organisations as companies that can be understood, measured and trusted over time. That is what ultimately attracts both regional and international capital. That is why mature public companies do not treat investor engagement merely as a marketing function when the sky is blue. The board, CEO, CFO, IR team and broader management also need to have the same view of the market’s expectations when the sky is grey.

GCC BDI: Looking ahead, what should boards prioritise to strengthen their capital markets narrative and access to investors?

Schutzmann: Based on conversations with company leadership and investors, I believe GCC boards would benefit from spending more time understanding who and what really drives their share price.

That starts with an outside-in perspective. Many boards still operate with outdated assumptions about what investors expect.

Some believe that earnings guidance is not allowed, even though all public Saudi banks now provide guidance. Others remain hesitant on strategy disclosure because they believe they will give away their competitive advantage. Many others still see no need for quarterly earnings calls, although the number of GCC earnings calls has risen from fewer than 10 companies a decade ago to more than 130 per quarter today, representing around 80% of total GCC market capitalization.

However, the deeper challenge is that many boards still look at the company mainly through the P&L, while institutional investors look at cash flows, moat and capital allocation. For example, many companies don’t seem to look at whether they consistently generate returns above their cost of capital. Only a few companies publish a dividend policy, not to mention a capital allocation policy.

Therefore, the priority needs to be to move from reporting activity to explaining value creation. Investors do not need a laundry list of everything the company is doing. They want to know the three or four key things that will make returns sustainable, where growth will come from, how capital will be used, and what management will do if market conditions change.

Valuation is ultimately the product of business model performance and trust in management capability.

What role does governance play in influencing valuation, transparency and long-term investor trust?

Governance is fundamental because it tells investors how a company will behave when tough decisions need to be made. Quite often, governance can sound like a compliance topic, but investors see it differently. They are trying to assess if the board will protect minority shareholders, if capital will be allocated responsibly, and whether management will be held accountable. If they have doubts on any of those points, they will either demand a lower valuation or could avoid the company altogether.

Transparency is part of the same equation. A well-governed company not only publishes more information, but also information that helps investors make buy, sell or hold decisions. That means consistent KPIs, explanations of what drove and held back performance, and enough forward-looking context to understand where management sees the business in 3-5 years.

Is Investor Relations a Front Office or Back Office Function?

Investor Relations often finds itself stuck in an identity crisis. Is it a compliance-driven back-office function, similar to accounting, tasked with disclosure and reporting? Or is it a strategic, market-facing role that actively drives shareholder value, placing it alongside front-office activities like sales or corporate strategy? The truth lies in IR’s core objective: to shape how capital markets perceive and value a company.

The question whether IR is a front office or back office function has implications for how companies deploy resources, define priorities, and measure their success. The key lies in recognizing IR’s unique ability to match a company’s performance with the capital market’s perception—an interplay that is central to value creation. Getting it wrong risks diminishing the value that IR can create for the company, its owners, and its management.

Investor Relations' Misunderstood Role

For many years, IR was seen as a function focused on reacting to market needs—preparing earnings reports, managing disclosure, and arranging annual general meetings. While these activities are important, they do not capture the transformative potential of IR in today’s complex capital markets. This compliance-first approach relegates IR to the sidelines, denying it the resources and authority to shape the company’s investment narrative proactively.

At its core, IR serves as the voice of the company to investors, analysts, and the broader market. This role has evolved substantially, driven by rising investor demands for transparency, the growing influence of ESG factors, increased scrutiny from institutional investors, and the increasing role of AI in the investment process. Modern IR is not merely about disseminating information; it is about shaping the company narrative. This means conveying how performance aligns with market expectations and, in doing so, influencing valuation multiples.

The Bridge Between Performance and Perception

To understand why IR deserves to be considered a front-office function, it is necessary to break down its role into two pillars: performance and perception. These pillars are not merely distinct areas of focus; they represent the interplay that ultimately determines a company’s valuation in the market.

Performance is the foundation of measurable operational and financial outcomes. Institutional investors look for companies with compelling strategies, disciplined capital allocation, and strong returns above the cost of capital. IR plays a central role in articulating these metrics to investors. For example, it demonstrates how a company is positioned in its industry, where its growth will come from, and how resources are being deployed to create value sustainably. Without IR translating these fundamentals into a cohesive narrative, the market risks undervaluing the company’s achievements.

Perception, on the other hand, is the multiplier effect. While performance builds the foundation, perception determines the valuation premium (or discount) that the market applies to a company. Investors trust companies with credible management teams that deliver on their promises and engage transparently. A mature IR function not only engages proactively with stakeholders but also articulates external expectations inside the companyTogether, these pillars of performance and perception define a company’s market valuation.

Earnings Equivalent Valuation Premium

Let’s take an example of an airline. The company trades at a P/E ratio of 10.4x, based on net income of USD 1.38 billion, giving it a market capitalization of approximately USD 14 billion. A more mature front office IR function which understands what information investors need, how they come to their valuations, and effectively communicates corporate strategy and capital allocation could potentially generate a valuation premium and improve the airline’s P/E ratio by around 15%, from 10.4x to 12x.

Key insight: IR can provide a far more efficient lever for value creation than operational improvements alone. A 15% improvement in P/E ratio through stronger market perception is equivalent to a 13.9% revenue increase—without adding a single dollar in operations.

The resulting valuation uplift would increase the airline’s market capitalization by USD 2.1 billion, a figure too big to be ignored in discussions of value creation by executives and the board. To achieve this hypothetical USD 2.1 billion uplift through operational improvements alone, the airline would need to grow its net income by USD 215 million. Given the company’s FY2023 net income margin of 25.8%, this would require an additional USD 833 million in FY2023 total revenue – or the equivalent of a 13.9% annual revenue increase. Achieving such growth in a highly competitive industry, where margins are constantly under pressure, would be far from easy.

{{statistics}}

This scenario highlights the outsized impact that IR’s ability to improve market perception can have on valuation. While operational performance will always remain the foundation, IR can provide a highly efficient lever for value creation. By positioning IR as a front-office function, companies like the airline example can unlock valuation premia, drive shareholder confidence, and achieve outcomes that would otherwise demand significant - perhaps impossible - operational improvements.

Designating IR as Front Office

Treating IR as a front-office function changes how the organisation creates value. It gives IR a strategic mandate, closer proximity to leadership and direct accountability for helping management understand and influence valuation outcomes. Companies that fail to recognize this strategic importance are leaving untapped value on the table.

When IR is seen as a strategic partner, its insights on market sentiment, investor expectations, and valuation drivers are not just heard but can proactively influence corporate strategy.

The capital markets reward companies with proactive IR functions. For investors, it signals that the company understands its audience and takes its market-facing responsibilities seriously. Internally, this shift elevates IR’s role, ensuring it is equipped with the resources, tools, and authority to make a meaningful impact on valuation.

Reimagining IR in Organizational Design

For IR to operate effectively as a front-office function, companies need to embed it more deeply into their organizational design. This means granting IR a seat at the table where strategic decisions are made and making it accountable for delivering insights that drive valuation.

A well-structured IR function should report directly to the CEO or CFO and have representation in executive committee discussions. This proximity allows IR to translate investor expectations into actionable insights for leadership, while also ensuring that corporate decisions are communicated effectively to the market. Regular internal board reporting - covering market sentiment, valuation analysis, and investor engagement metrics – then ensure IR’s contribution is recognized and informs strategic planning.

Next to finance, IR must also integrate with other key functions, such as strategy, business lines, and ESG. As ESG concerns grow, IR’s role in articulating the company’s sustainability narrative becomes critical. This collaboration ensures that the company’s story resonates with the expectations of long-term investors, who increasingly prioritize these non-financial factors.

The Broader Implications for Companies

Designating IR as a front-office function also changes how companies measure and reward its success. Instead of focusing solely on disclosure accuracy or internal feedback, companies should evaluate IR’s impact on valuation. This better reflects IR’s strategic contribution and aligns with its role as a pillar of shareholder value creation.

The benefits of the shift are obvious. Companies that treat IR as a strategic, market-facing role tend to attract long-term, stable investors and achieve higher valuation premiums. By proactively managing the investment narrative and aligning external with internal expectations, these companies are also better equipped to meet sell-side analyst forecasts and buy-side expectations.